Why Is Kemet Stock Down Tody Again

A couple of shares we have been post-obit as candidates for the SHU portfolio have seen quite some momentous downwards movements. And so, we wonder whether information technology's getting time to execute and take a position.

Commencement one up, KEMET Corporation (NYSE:KEM). Expect what is happening here, this own't pretty:

In fact, we wrote an commodity in Baronial arguing that it should rebound (with the stock then at $23 and change), which information technology did, merely then it crashed lower. We also argued in that article that the one take chances would be an escalation of trade tensions between the US and China.

Well, trade tensions between the U.s. and People's republic of china did happen. Unfortunate, equally the visitor had just gone into a joint venture in Cathay (from the Q1 10-Q):

On January 29, 2018, KEC entered into a joint venture agreement (the "Agreement") with JIANGHAI (Nantong) Film Capacitor Co., Ltd ("Jianghai Film"), a subsidiary of Nantong Jianghai Capacitor Co., Ltd ("Jianghai") for the formation of KEMET Jianghai Electronic Components Co. Ltd., a limited liability company located in Nantong, China. KEMET Jianghai Electronic Components Co. Ltd. was officially established on May xvi, 2018, and volition manufacture axialelectrolytic capacitors and (H)EV Film DC brick capacitors, for distribution through the KEMET and Jianghai sales channels. KEC and Jianghai Film will each provide initial capital contributions through a combination of greenbacks and manufacturing equipment, and will be as represented on the joint venture'south board of directors.

And it does have production facilities in Cathay (from the 10-Q):

KEMET operates twenty-four production facilities in Europe, North America, and Asia, and employs approximately 14,750 employees worldwide. Commodity manufacturing previously located in the United States has been essentially relocated to our lower-cost manufacturing facilities in Mexico, Mainland china and parts of Europe. Production remaining in the United States focuses primarily on early-phase manufacturing of new products and other specialty products for which customers are predominantly located in North America. Nosotros besides have low cost manufacturing facilities located in Vietnam and Thailand.

Information technology's useful to come across what management said nearly the situation (from the Q1CC):

Offset of all the tariffs are not that larger for us, we're not importing all that much from China into the Us, just also we're passing that on ...

The products we export from China to the United Stated are Film products from Anting, Tantalum Polymer from Suzhou and Magnetic, Sensors and Actuators from Chowmin [ph]. In the effect, this situation is non expeditiously resolved we're looking into alternative locations to movement production heading to the U.s. out of China.

That was virtually the possible new tariffs (some of which now seem to have materialized in the batch of v% or ten% on $200 billion of The states imports from People's republic of china).

But KEMET was already hit by the first batch of Us tariffs on $60 billion of imports from Communist china. However, the visitor just passed on these costs (from the Q1CC):

Nosotros volition pass entire cost onto our direct customers and distributors which will be reflected every bit a line item on the invoice. We have experience[d] no push back and have already begun to receive such payments.

So this is why there wasn't much of a share price reaction, merely plain, passing on the new tariffs is less of an option. Instead, management was prepared to shift production to new locations:

Options currently under consideration are moving The states designated magnetic and sensors production from Chowmin [indiscernible] China, Ho Chi Minh City, Vietnam and Tantalum Polymer from Suzhou, China to Victoria, United mexican states and or Bangkok, Thailand. And Moving-picture show products from Anting, China to Bulgaria and Republic of macedonia.

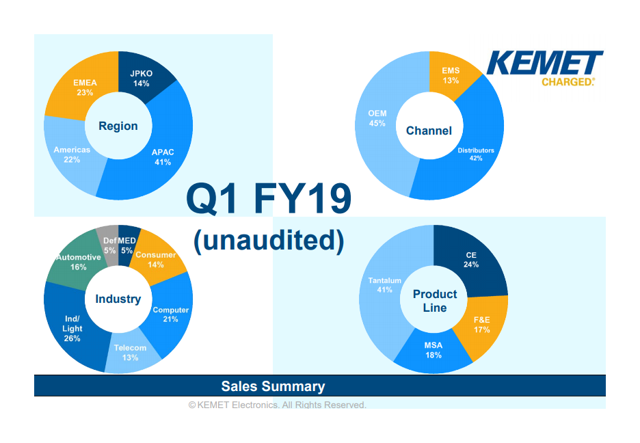

From the September Rodman & Renshaw Investor Presentation:

That 41% Tantalum might be a source of problems. Here are some items on the official The states government list that might be relevant:

- 2615.90.thirty Synthetic tantalum-niobium concentrates

- 8103.20.00 Tantalum, unwrought (including bars and rods obtained but past sintering); tantalum powders

- 8103.30.00 Tantalum waste and chip

- 8103.90.00 Tantalum, articles nesoi

However, Tantalum Polymer doesn't seem to be on the list. The other product descriptions from the KEMET Q1CC aren't specific plenty ("magnetic and sensor production" "film products") to notice whatever exact matches in the list of tariffs.

And in fact, it doesn't matter all that much, as these tariffs are gear up to go to 25% by the end of the year, and there could very well exist a new round after which basically all US imports from Cathay face up tariffs. If that happens, the company-specific problems having to relocate production could simply exist dwarfed past the decline in market place sentiment, which is already shaky later bond yields started to rising again.

Why practise we say that? Well, here is Kevin Hassett (from USCHNews):

"If I were a business, I would basically just stay abroad from People's republic of china right now. Their misbehavior is and then terrible." Kevin Hassett, chairman of the Council of Economic Directorate said on Yahoo Finance'due south Market Mover Friday. "That's why President Trump is taking a difficult line with them. They've got to change the way they behave if they want to exist part of this modern earth global economy."

The market is slowly coming effectually to the likelihood of a prolonged merchandise state of war with Cathay. While that is an undisputed negative for the market, some companies are more than affected than others, and it stands to reason that KEMET is in the firing line.

Chinese Market

Apart from having to relocate some production and/or pass on tariffs to customers, the company besides sells to China. In the above diagram, it shows that Asia-Pacific is its well-nigh of import region with 41% of sales, simply we could not detect a finer geographical breakout on the country level.

Given the industries involved, the Chinese market is likely to exist considerable for the visitor though (from the Q2 2018 CC):

A sizable portion of POS growth came from new customers in Prc and Taiwan as nosotros go on to expand our customer base at that place with a focus on magnetics, sensors and actuators and specialty products... The industrial segment is positive. This is more often than not driven past Red china and a reinvigorated economical situation in Europe, which remains our principal market for this segment. Telecom continues to show general weakness among the European players, while we and they wait for the 5G investments to boot in. We are, however, expecting that to be driven mainly out of China.

Also here (from the Q4 2018 CC):

Regarding telecomm, there is excitement for the 5G deployment in China where we exercise expect the first standard improver of the 5G protocol to be launched around June. This will exist some other key driver for demand for our products.

Not only 5G, it'due south also EVs that are a boon to KEMET's products (inverters and capacitors), and Cathay is betting large on EVs (from the Q3 2018 CC):

The JV will give us an opportunity to meliorate our manufacturing footprint in China, which of class is where most of these cars are being produced and solid today. Too it gives us an opportunity to log into their supply chain, which will improve not just the JV toll operation, but besides our cost performance overall. So we believe we can improve the margins in this segment and we believe we have applied science that we can use in these segments and nosotros believe that there will growth over the next several years in this expanse. We would similar to be a part of that.

IoT and Industry are the other primary demand sources for the visitor's products.

Here is another way to gauge the importance of Communist china for KEMET. These are its Asian sales offices (from the company website):

And these are its E Asian distributors:

And so the upshot is that China is both increasing in importance every bit a production location as well equally a marketplace for finish products, and so the risks fastened to the escalation of the trade war tin't be underestimated.

Even without having exact figures of the importance of Chinese sales or production facilities, these aren't likely to be insignificant.

Nosotros tend to the opinion that Mainland china, given its ambition in high-tech industries, isn't likely to put too many barriers to critical products and technologies, as that could hinder its own progress in these advanced sectors.

The company has 53 patents, so some products might be difficult to replace. Autonomously from that, the MLCCs are really in short supply.

The stock price

KEMET stock is already downwardly much more than than the overall market, so we think most of the issues should be priced in by at present. Remember that the need for MLCC (multi-layer ceramic capacitors) is outstripping supply, and direction foresees no change in this situation anytime soon.

In fact, information technology'due south increasing CapEx to deal with the surge in demand, and it will gradually introduce price increases every bit current contracts expire.

In the graph above, you see that the stock toll has already fallen to a support level at roughly $17, and if that breaks, the adjacent level looks to be $15:

Valuation

KEM PE Ratio (TTM) information by YCharts

KEM PE Ratio (TTM) information by YChartsDecision

The shares of KEMET accept fallen off a cliff, with the shares down to very reasonable valuation levels. Per management, they don't import all that much from Prc into the The states, and they tin can at to the lowest degree in part pass on the tariff into pricing.

What we do know is what the U.s. imports from China, and direction argued that it can either pass on tariff price to terminate consumers and/or shift production to other locations. The latter cost can be considerable, but are mostly one-off.

But that's not all the potential damage, KEMET can also be injure from Chinese retaliatory actions. The visitor does have sales to China, and although nosotros could not establish with whatever kind of precision how important the Chinese market is for the company, nosotros're fairly sure it is not insignificant. Nor practise we know exactly, given the land loftier-tech ambitions, how likely it is that Chinese retaliatory measures are going to exist a real problem for the company.

Nosotros take some comfort from the short supply in MLCCs. China isn't going to find replacements should tariffs harm KEMET's, only for other products, we're less certain how easy information technology is for the state to find alternative sources.

What'due south more, if the merchandise war really escalates, there are added incentives for the Chinese to reverse-engineer critical parts and not worry much near patent infringements in order to go less dependent on foreign engineering. That would be ironic, as it's the verbal opposite of 1 of the stated aims of The states policy towards Mainland china.

We call up that all but the worst-instance scenario is more or less priced in the shares at these levels though. Only and so again, the worst-example scenario (an all-out trade war between the Us and China) can't actually be ruled out with whatsoever kind of conviction.

This commodity was written by

Finding the adjacent Roku while navigating the high-risk, high reward landscape

I'm a retired academic with three decades of experience in the fiscal markets.

Providing a market service Shareholdersunite Portfolio

Finding the next Roku while navigating the high-risk, high advantage landscape.

Looking to discover pocket-size companies with multi-bagger potential whilst mitigating the risks through a portfolio approach.

Disclosure: I/we accept no positions in whatsoever stocks mentioned, but may initiate a long position in KEM over the next 72 hours. I wrote this article myself, and information technology expresses my own opinions. I am not receiving compensation for information technology (other than from Seeking Blastoff). I have no business concern relationship with any company whose stock is mentioned in this commodity.

Source: https://seekingalpha.com/article/4210576-kemet-corporation-is-falling-off-cliff

0 Response to "Why Is Kemet Stock Down Tody Again"

Post a Comment